Market Insights

Being Uncertain Is Wiser Than Being Certain | February 2024

Market Insights

Market Insights

February 14, 2024

Shapiro - February 2024 Market Insights

Being Uncertain Is Wiser Than Being Certain

At the beginning of 2023, most economists were certain that higher interest rates would slow the economy, cause unemployment to go up, create a recession and slowly bring down inflation. Wrong, wrong, wrong, and wrong. Instead, GDP grew a very healthy 2.5%, over 2.7 million new jobs were created with unemployment at near a record low of 3.7%. The inflation rate dropped from 6.5% and based on the Feds PCE, Personal Consumption Expenditures, is running at under 2% over the last 6 months.

Pause right there, and let that sink in. No wonder the stock market keeps setting records.

Chairman Powell recently said: “This is a good situation. Let’s be honest. This is a good economy. We do expect growth to moderate. Of course, we have expected it for some time, and it hasn’t happened.” The Atlanta Feds GDPNow is forecasting 4.2% for Q1 as of February 1.

The only thing for which I am certain is change. I am reading a book called Uncertain by Maggie Jackson. It is about the wisdom and wonder of being unsure. I am often quick to make up my mind and this new way of thinking causes me to challenge my assumptions and leads to better decisions. We live in a VUCA world, volatility, uncertainty, complexity, and ambiguity. There are numerous risks to this economy and there will be surprises. Let’s hope, they are positive.

Chairman Powell was recently discussing interest rates and how they affect the economy. “People will be writing papers about that 10 years from now and still fighting about it … it’s going to be uncertain.” For the record, I said this last month in January’s Market Insights.

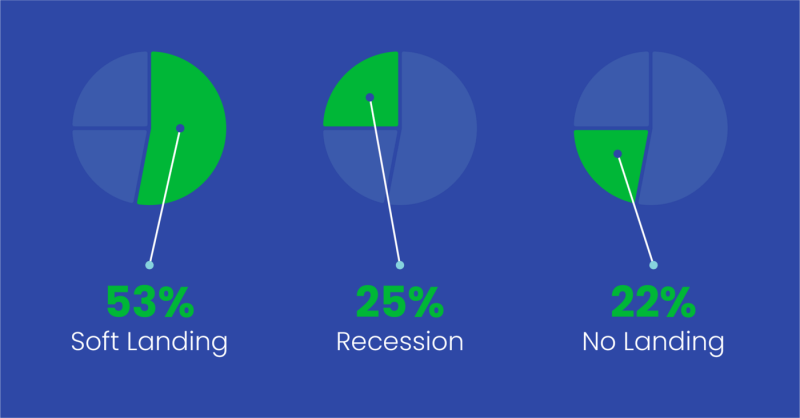

Thank you for voting last month on your predictions of what you thought the economy would do in 2024.

And the survey says…

53% voted for a Soft Landing

22% for No Landing

25% for a Recession

Inflation

The Inflation Fight is Still On

The Consumer Price Index (CPI) rose in January 3.1% down from December 3.4% on an annual pace. It sounds good but economists were expecting it to be 2.9%. The Core CPI, excluding food and energy, was about the same as December. Shelter costs and services were expected to fall in January and didn’t. Shelter was the single largest contributor to January inflation along with increases in medical care and transportation. Supercore is the inflation sector of CPI which the Federal Reserve watches closely and includes core services costs minus housing. That showed a reacceleration from the prior year to the fastest pace since May. On a monthly basis, prices rose at their fastest rate since April 2022. It continues to be a bumpy ride to bringing inflation down to 2%, no matter how you measure it.

Personal Consumption Expenditures (PCE) is the Fed’s preferred inflation measure. December was reported at the end of January and was very positive. December closed out a year in which inflation declined markedly. Prices were up 2.6% on the year, down from the 5.4% increase at the end of 2022. Core prices, which exclude volatile food and energy costs, rose 2.9% on the year, a slowdown from the prior month. This is almost a 3 year low.

On a three-month annualized basis, core PCE inflation, excluding food and energy, slipped to 1.5% in December from 2.2% in November. On a six-month basis, it was 1.9%, unchanged from November. Both figures are below the Fed’s 2% inflation target.

The Producer Price Index will not be out until Friday.

Manufacturing

Positive to Steady

The ISM Manufacturing index rose to 49.1 in January up from December 47.0. It is still in contraction but a strong gain. The best news comes from the new orders index, which moved into expansion territory for the first time in seventeen months. Meanwhile, output remained stable as the production index ticked up to 50.4. Also, the ISM Non-Manufacturing service index rose to 53.4 in January, beating even the most optimistic forecast from any economics group on Bloomberg. We will see if this trend of expansion continues.

Orders for core capital goods (excluding aircraft and transportation), which will lead to shipments in the future, were up a healthy 0.6% in December versus a consensus expected gain of 0.2%. Including transportation, December was the same as last month. In the past year, orders for durable goods were up 4.8%, while orders excluding transportation were up a more modest 2.3%.

Shipments of “core” non-defense capital goods excluding aircraft, an essential input for business investment in calculating GDP and a leading manufacturer indicator, rose just 0.1% in December. Shipments have been trending down for 2 years.

New home sales recovered in 2023. Lower mortgage rates, now down to 6.6%, and lower home prices due to building smaller houses have helped. Despite a general downward trend since the summer, sales activity for 2023, as a whole, was up 4.2% from the previous year. This is the first annual gain since 2020 when COVID shutdowns and work-from-home spurred a boom in demand for single-family homes.

U.S. Nonresidential Construction spending continues to be strong and near its high. New light-vehicle sales totaled 15.46 million units in 2023, up 12.4% from 2022. January sales were down slightly at a 15 million annual rate.

The Shapiro Nonferrous Scrap Activity Index, which tracks our daily purchases from the duplicate accounts across our ten locations and a diverse industrial base, fell in January and was 9% below our twelve-month trailing average. There was some bad weather noise in the January number.

China

Certain and Wrong

I was certain that with the over 30% drop in construction spending, a very intensive metals sector, metals consumption had to drop. Wrong. Base metals consumption and production grew again last year. Most base metals prices were up 5% or greater for the year. The green sector of manufacturing, EVs, solar panels, wind equipment, charging stations, transmission cables, and data centers offset much of the housing downturn.

Amazingly, China’s aluminum production and consumption has continued to grow even during the pandemic and the housing implosion. China consumes 62% of the worlds primary aluminum and produces 59% of the world’s aluminum. The negative balance is made up from imports, much of it from Russia.

China’s economy is large and diverse. Its economy continued to grow at 5% last year. The manufacturing PMI is still in contraction at just over 49 and the Caixin manufacturing index came in at 50.4 just in expansion and nearly the same as December. 50 is the dividing line between expansion and contraction.

China’s economic reporting cannot be taken at face value. They report their employment rates only from large cities and anyone who works 1 hour per day is counted as employed. China didn’t like that youth unemployment was too high. They quit reporting it. Consumer confidence is not reported but service spending continues to fall. House prices keep falling and inflation is close to zero. “Figures don’t lie but liars’ figure.

PCSD, Post Covid Stress Disorder, will continue to hurt their economy for years. A reflection of this is the recent heavy selloff in China’s benchmark stock market CSI 300 Index which brings its plunge to a brutal 40% over the past three years.

Metals

2024 Aluminum Forecast

This is my favorite metals report. I rely on much of my aluminum information thanks to Edward Meir emeir@marex.com. I subscribe to his daily, monthly, and annual analyses. He has been recognized as one of the most accurate metals forecasters in the country. I also subscribe to Harbor, who have correctly called the bear market of the last few years.

Ed Meir’s detailed analysis covers global macro trends from China, US, and Europe, which he sees as neutral to bearish. He points out that if China were to correct their massive property debt issues, all base metals could rally. So far Beijing has shown no interest in changing its policies. Other forecast factors he analyzes are the US economy, interest rate, and inflation plus supply/demand, metal producers, inventories, Russian metal, geopolitics, EVs, and US infrastructure spending. This could be a dissertation.

After considering all these factors, this is his forecast along with other analysts. Hope it helps with your budget planning.

Prime aluminum prices for February dropped 2 cents a pound and prime scrap prices rose about 3 cents a pound due to increased demand and lower supplies. Secondary aluminum aero turnings rose 4 cents a pound. Copper, nickel, and stainless steel prices were about unchanged. Scrap steel was down slightly. I plan on being less certain and more uncertain this year. I believe it will improve my decision-making process. |

P.S. I invite you to read our new segment at the end of each month’s Market Insights. It aligns with Shapiro’s purpose of Making the Planet Better Together. Shapiro has launched Circular by Shapiro (circularasaservice.com) to provide the environmental metrics and data needed to reach sustainability goals. Below, you will find Sustainability Insights. |

“The reality is that tomorrow is most certainly uncertain, and no matter how many expectations we form, tomorrow will come, tomorrow will go, and it will all be what it will be”

Lori Deschene

“Life is good. Family and health are precious.”

Bruce Shapiro

Sustainability Insights by Maddie Carlson

February 2024 Market Insights

What would happen to your company, product, or process if the material for one part was no longer available? At the current rate of extraction, we are depleting the planet’s finite natural resources to where we are at risk of this question becoming a reality.

The rate of extraction can be tracked by the changes in the Earth Overshoot Day. This day is the calculated date when humans have used up more natural resources than can be reproduced in a year. Predictions for 2024 indicate that the day will be July 27th, 157 days ahead since it was first tracked in 1970. At this rate, natural resource consumption is not sustainable.

Manufacturing is known for its resource-intensive processes that rely on non-renewable materials like fossil fuels, metals, and minerals. The environmental toll of extraction, transportation, and processing increases carbon emissions and land destruction. To mitigate these adverse effects, a shift towards sustainable manufacturing is crucial. Creating 100% recyclable products and reusing each material will be necessary to end over-extraction.

A shift to circular practices will help the environment as well as the economy. As finite resources diminish materials are vulnerable to drastic price increases or become nonexistent altogether. A constant stream of recycling and reuse would ensure the available and price stability of materials compared to dependency on primary materials.

A circular program would lessen the stress on the environment, economy, and supply chain. A life-cycle analysis is a great first step to highlight opportunities to implement circular practices.

Thanks for Reading.

Not a subscriber? Sign up below.