Market Insights

Inflation Confusion | April 2024

Market Insights

Market Insights

April 11, 2024

Shapiro - April 2024 Market Insights

The Truth About Inflation Confusion

“Inflation is when you pay $15 for the $10 haircut that you used to get for $5 when you had hair.”

Sam Ewing

Consumers are pissed off about high prices and yet consumer spending continues fueling the economic growth. Their sentiment these days is “WTH! If inflation is cooling why are my grocery bills still so high?” “These prices make no sense, and I can’t believe inflation is at only 2.5% to 3%.” “Why aren’t prices falling.” “It’s just not right.”

We certainly have a right to be angry. For consumers, the reality is this: The same cart of groceries that cost $100 in December 2019 now costs $135 depending on store and food preferences. No one likes paying higher prices and we remember what prices used to be before the pandemic. How did this happen

The pandemic started in March of 2020. Unemployment soon skyrocketed to 14.8%. People were in quarantine. The economy looked like it was falling into an abyss. The vaccine was not yet developed, and hospitals couldn’t handle all the Covid patients. Hundreds of thousands of people were dying, and that number reached over 1,200,000. In July 2020, Congress distributed $2 trillion dollars to individuals and businesses to ease the pain of lost income. By the end of the year a vaccine was miraculously developed, and life started to return to normal. Remembering what happened in 2020 helps me understand the reasons for the inflation confusion.

The pandemic has had a significant impact on inflation. Fewer people went back to work causing a labor shortage and this drove up wages in all industries. Food prices were driven up by increased fertilizer prices, labor, and transportation costs. The Putin war also caused worldwide energy prices to spike. Gas in the US rose to close to $6.00 a gallon. There continue to be famines, floods and droughts everywhere driving up food prices. In addition, corporate greed sent and kept food prices higher along with shrinkflation, the trickery of less chips in the same size bag.

Inflation or Corporate Greed?

Here’s my research on food inflation. The volumes of soda, cereal, candy bars, paper items and beef are all down. The prices for these same products are up 40% to 60%. The largest companies have found that they can charge these much higher prices and make more. Grocery store chains have also raised their prices over inflation and are reporting record profits.

This is known as sellers’ inflation. According to the Kansas City Federal Reserve corporate profits have accounted for 40% of higher inflation. Other analysts say the profits amount to over 50% of inflation. No wonder the stock market is doing so well.

CPI inflation fell by 3.1 percentage points last year, from 6.5 percent in December 2022 to 3.4 percent in December of 2023. Lower inflation does not mean that prices will come down. And remember, US inflation is lower than any country in the western world.

Are you better off? Yes. Does it feel like it? No.

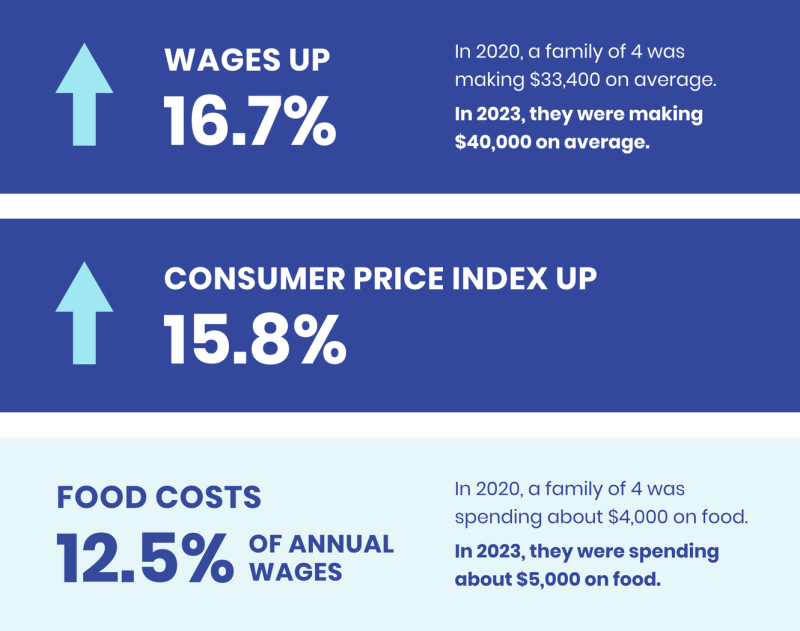

This graph puts food inflation into perspective. Inflation measured by the Consumer Price Index has gone up 15.8% in the last four years. Wages as measured by private industry have gone up 16.7%. The average family of 4 in 2020 was making $33,400 per year and spent 12% of their wages on food or about $4000. With the 16.7% wage increase over the last 4 years, the average family of 4 in 2023 is now making $40,000 per year [CPI increased 15.8% in the same time frame]. That same family spends about the same 12% of their income on food and groceries, about $5400 [rounding up]. Food prices did go up 35% on the high end, about $1400 a year, but wages increased $6600 per year. That leaves $5200 pretax to cover the rest of inflation.

Here are other reasons the economy is stronger, and spending is greater:

- Even with higher food costs and inflation, consumer confidence is higher now than a few years ago

- The Dow Jones has gone up 50% in the last 5 years

- The NASDAQ has doubled over the same time period

- 401K plans have also appreciated

- Interest rates paid to consumers is near 5%

- Home values have risen for all homes, condos, etc. across the US from an average of $242,000 to $346,000 in the last 4 years

After analyzing this data, the facts are that inflation is falling, the economy is strong, jobs are plentiful, and the unemployment rate is 3.8%. Hedgehogs (see March 2024 Market Insight) don’t see it this way. After considering the information above, those who disagree may want to spend their time reading the Wall Street Journal.

Inflation

Inflation is still sticky

- The Consumer Price Index (CPI) for March was slightly higher than expected. The core CPI gauge, which excludes volatile food and energy prices, on an annual basis was unchanged from last month at 3.8%. On a month over month basis core CPI topped forecasts for a third straight month, with a 0.4% increase that was the same as the last 2 months. Headline CPI rose 3.5% down slightly from 0.4% last month but up on an annual to 3.5% from 3.2%, boosted by higher energy costs.

- The super core CPI measure, services prices excluding energy services and housing costs, that the Fed has highlighted, rose 0.6% in March after increasing 0.5% in February and 0.8% in January. The March measure was driven by higher prices for motor vehicle insurance (+2.6%) and medical care services (+0.6%). In the last twelve months, the super core measure is up 4.8% and has been accelerating as of late. With this information the anticipated June interest rate cuts are dimming.

- Personal Consumption Expenditures (PCE) is the Fed’s preferred inflation measure. February was reported at the end of March. It rose 0.3% in February, bringing the twelve-month comparison to 2.5% (from 2.4% last month). “Core” prices, which exclude the ever-volatile food and energy categories, also rose 0.3% in February and are up 2.8% versus a year ago. “Supercore,” which is services only (no goods), excluding food, energy, and housing rose 0.2% in February and is up 3.3% versus a year ago. Services inflation excluding housing and energy, dropped to 0.2% from 0.7%.

- The Producer Price Index [PPI)] for February “core” prices rose 0.3% following an outsized 0.5% increase in January. Core prices have eased since peaking at 9.7% back in March of 2022, and are now up a moderate 2.0% from a year ago. March will be released in a few days.

- Federal Reserve Chairperson Powell recently commented on the pickup in inflation in January and February. “The recent data do not…materially change the overall picture, which continues to be one of solid growth, a strong but rebalancing labor market, and inflation moving down to 2% on a sometimes-bumpy path,” he said. Currently there is a 50% chance that he will lower rates by 0.25% in June. If the economy continues to be as strong as it is, the Fed may delay interest rate cuts.

Manufacturing

ISM breaks into expansion

The ISM Manufacturing index broke into expansion [50 is the dividing line between expansion and contraction] for the first time since September 2022. March rose to 50.3 from 47.8 in February. Demand is in the early stages of recovery, and new orders broke into expansion for the first time in 19 months. The price index has been in expansion this year after being in contraction most of last year. The ISM Non-Manufacturing service index fell slightly again to 51.8 from 52.6 in February. The GDPNow forecast produced by the Atlanta Fed estimates that the Q1 economy is now tracking at a 2.3% growth rate above the 1.2% forecast from last year. Q4 growth rate was 3.4%.

- Orders for core capital goods (excluding aircraft and transportation), which will lead to shipments in the future, rose 0.5% in February after they declined 0.3% in January.

- Shipments of core non-defense capital goods excluding aircraft, an essential input for business investment in calculating GDP and a leading manufacturer indicator, declined 0.4% in February. If unchanged in March, these orders would be up at a 1.9% annualized rate in Q1 versus the Q4 average. This is still good news even though shipments have been trending down for the last 2 years.

- Housing remains steady with the lower interest rates and falling prices of new homes. Existing home values rose over 6% in the last year.

- Car and light truck sales were down slightly from February and still at 15.56 million units per year.

- U.S. Nonresidential Construction spending dipped slightly but is still near its high.

- The Shapiro Nonferrous Scrap Activity Index tracks our daily purchases from the duplicate accounts across our ten locations and a diverse industrial base. March volumes were very close to February and were right on track with our twelve-month trailing average.

China

Will China continue to pick up?

After 5 months of contraction in manufacturing, the March indicators have gone above 50, which is in expansion, while under 50 is contraction. This was led by the manufacturing sector, with exports exceeding expectations and industrial profits returning to growth.

The official PMI (Purchasing Managers Index) expanded for the first time in six months to 50.3. The private manufacturing index Caixin, rose slightly to 51.1. The data showed that the industrial manufacturing sector is the bright spot. China believes it can revive its economy through exporting its products. However, that Chinese strategy is called dumping. They did that decades ago and more than 2 million Americans lost their jobs. This will not happen now because the US and the EU will put in strong tariffs to stop this.

China’s problems are the property crisis, struggling consumers, disinflation, and geopolitical tensions. The elephant in the room is the ongoing property debt crisis which is not close to being resolved. Bad debt continues to pile up. Many property companies should have gone into bankruptcy but haven’t. If they did, property values of existing homes would plummet causing a major financial crisis. Until this is resolved, it will be very difficult for China to climb out of its hole.

Ray Dalio is the billionaire founder of Bridgewater. He has had a personal relationship with President Xi for decades. Years ago, Dalio had praised Xi for surrounding himself with good advisors who would challenge him and debate the central issues. This is no longer true as Xi has terminated any dissenters. Dalio now warns that China should cut its debt and ease monetary policy or face “a lost decade.” Don’t keep your fingers crossed.

Metals

A Brighter Aluminum and Copper Outlook

On March 24, Goldman Sachs said that they see interest rate cuts this year leading to higher aluminum, copper, and gold prices. This is based on what has happened in growing economies, with no recessions when the rates are cut. Along with other commodity forecasters, they say commodities are entering a fresh cyclical upswing aided by tighter supplies and an upturn in the global economy. In Goldman’s year-end forecasts for 3-month LME, copper was seen at $10,000 a ton, aluminum at $2,600 a ton, and gold at $2,300 an ounce, which would be a nominal record. Goldman has generally been more bullish than other analysts, so we’ll see. Century Aluminum has announced plans to build a Green Aluminum Smelter Project. It is the first new US aluminum smelter in 45 years and will be in the Ohio/Mississippi River Basin area. The plan is to produce over 570k metric tons per year by the end of the decade. They received approval from the Department of Energy for the project. This will make the US less reliant on offshore imports. It is being funded by a $500M grant from the US Inflation Reduction Act. Prime aluminum rose from March by 4 cents along with prime scrap. Secondary scrap remained the same. These prices are up about 9 cents a pound from January even though LME aluminum has not changed. This reflects the scrap shortage which is also being caused by the export demand for scrap. Copper went up about 7%. Nickel fell while stainless scrap was up for 304 grades. Steel prices are neutral for April after falling in the last 2 months. Despite the volatility, uncertainty, complexity and ambiguity, the US economy continues to do better than forecasted and inflation is improving. Amen. |

P.S. I invite you to read our new segment at the end of each month’s Market Insights. It aligns with Shapiro’s purpose of Making the Planet Better Together. Shapiro has launched Circular by Shapiro (circularasaservice.com) to provide the environmental metrics and data needed to reach sustainability goals. Below, you will find Sustainability Insights. |

“Inflation destroys savings, impedes planning, and discourages investments. That means less productivity and a lower standard of living.”

Kevin Bacon

“Life is good. Family and health are precious.”

Bruce Shapiro

Sustainability Insights by Maddie Carlson

April 2024 Market Insights

I’ll Have Some Fries With My Debit Card

Did you know that every molecule of plastic ever created still exists on Earth today? Plastic takes at least 500 years to break down, so it never truly disappears. Instead, it breaks down into smaller units known as microplastics. These microplastics can be found everywhere, from the bottom of the ocean to the snow on Mount Everest and even in human blood! In fact, research suggests that we consume around 39,000 to 52,000 microplastic particles each week through the air we breathe, the water we drink, and the food we eat. This amount is equal to eating one plastic debit card a week.

All plastic items contribute to the creation of microplastics, including plastic bags, bottles, food storage containers, cutting boards, polyester clothing, glitter, and resin products. Although the extent of microplastics’ health effects is still being studied, it’s best to avoid them as much as possible. By making a few simple changes, such as using a wood cutting board, glass containers, dusting frequently, using an air filter, washer drain filters, and cutting out plastic waste bottles, we can all help to reduce our exposure to microplastics.

Exciting research reveals that enzymes and worms can decompose plastic into its original components. This would not only decrease microplastics and their harm but also create the potential to create new plastic without new resources. This breakthrough could significantly reduce the impact of plastic waste on the environment and pave the way for a more sustainable future. Until then, we can make meaningful environmental impacts by reducing plastic consumption and consume only a half a credit card.

Please reach out if you have any questions on eco swaps for your plastic products!

Thanks for Reading.

Not a subscriber? Sign up below.