Market Insights

Whoops! Forecasts Vs Reality | November 2023

Market Insights

Market Insights

November 15, 2023

Shapiro - November 2023 Market Insights

WHOOPS! FORECASTS VERSUS REALITY

|

|

Inflation

Forecast:

“TO GET INFLATION DOWN TO 2% “WE MAY NEED TO TOLERATE UNEMPLOYMENT OF 6.5% FOR 2 YEARS.” JASON FURMAN SEPTEMBER 2022

Reality:

INFLATION IS MOVING TOWARDS 2% AND UNEMPLOYMENT IS AT 3.9%

That inflation quote above was made fourteen months ago by a well-respected Harvard economist, Jason Furman. Whoops! Inflation has been approaching 2% over the last four months, and unemployment is 3.9%. When economists talk about inflation, they mean the rate at which prices change, whether up or down. Right now, we have disinflation, meaning the speed is trending down. The data and statistics used to measure inflation listed below are all moving down and towards the 2% target.

- The Consumer Price Index (CPI) was flat in October, and rose only 3.2% from a year earlier, down 0.5% from last month. The Core CPI, excluding food and energy, rose 0.2%, down 0.1% from last month and increased only 4% from a year earlier, the smallest annual change since September 2021. Core inflation for the five months ended in October was at a 2.8% annual rate. According to Chicago Fed President Austan Goolsbee, the 12-month inflation rate is on track this year to have posted its largest slowdown in at least four decades. “We may have brought down inflation as fast as it has ever come down, and we did that without starting a recession.”

- The Producer Price Index in October for final demand dropped a whopping 0.5 percent, after advancing 0.4 percent in September on a seasonally adjusted basis. The October decline is the largest decrease in final demand prices since a 1.2-percent drop in April 2020. On an unadjusted basis, the index for final demand rose 1.3 percent for the 12 months ended in October. Core PPI rose only 0.1% in October and for the year is up 2.9%.

- Personal Consumption Expenditures (PCE) is the Fed’s preferred inflation measure and is reported at the end of every month for the prior month. For September, core inflation, excluding food and energy, was 0.3% versus August’s 0.1%. Core prices were up at a 2.8% annualized rate in April through September, down considerably from a 4.5% annualized rate in the prior six-month period. The Fed’s inflation target is 2%. The report using the PCE measures shows inflation is getting close to 2% on a short-term basis.

- Employers added 180,000 jobs in October, and job openings held steady at 9.6 million. The unemployment rate was up 0.1% to 3.9%. As inflation has declined, so have pay increases. For October, average hourly earnings were up 4.1% from a year ago versus the year-over-year gain of 4.9% last year, in October 2022. Those numbers prevent any upward spiral in wages and inflation and are consistent with the Fed’s 2% inflation target.

Manufacturing

Continuation of Mixed Signals

When speaking with the Shapiro manufacturing base, most say demand is still good but faces a shortage of dependable workers. The manufacturers operate at an elevated level but need entry level workers to reach total capacity. Even with increased wages and an improved rate from 2022, turnover remains high with this entry-level group. Manufacturing will continue to stay level unless a recession ensues.

- The Manufacturing PMI measures manufacturing activity across eighteen types of industries, from food, plastics, metals, and others, fell in October by 2.3 to 46.7. Economic activity in manufacturing contracted in October for the 12th consecutive month following 28 months of growth. Just two out of eighteen major industries reported an increase in October. Survey comments cited weakening demand, slowing activity, and dwindling optimism for 2024. Weakening demand was most easily seen in the new orders index, which remained in contraction for the fourteenth consecutive month and further into contraction.

- Orders for core capital goods (excluding aircraft and transportation), which will lead to shipments in the future, rose a healthy 0.5% in September after 0.5% gains in August and July. In the past year, orders for durable goods are up 3.8%, while orders excluding transportation are up a modest 1.1%.

- Shipments of “core” non-defense capital goods ex-aircraft (an essential input for business investment in calculating GDP and a leading manufacturer indicator) were the same in September. These shipments rose at a 1.3% annualized rate in Q3 vs the Q2 average. Industrial production was strong again in September, up 0.3%, rising at a 5.2% annualized pace in the past three months versus just 1.8% annualized over the past six months and 0.1% in the past year.

- The housing market continues to confound me. The number of homes under construction is hovering near the highest level on record back to 1970. Yes, and the average price of houses is also near the top, along with mortgage rates of about 8%. There has been a housing shortage for some time. Few existing homes are for sale. Even though renting is a significantly better value, there is still strong housing demand.

- U.S. Nonresidential Construction spending continued to grow slightly in September and is at a new high.

- New light-vehicle sales in October were 15.5 million, down slightly from 15.7 million last month, despite the higher prices of cars and borrowing costs.

The Shapiro Nonferrous Scrap Activity Index, which tracks our daily purchases from the duplicate accounts across our ten locations and a diverse industrial base, fell slightly from September, and was even with our twelve-month trailing average.

China

Little to No Good News

China’s official PMI manufacturing index fell into contraction in October to 49.5 from 50.2 in September. The Caixin/S&P Global manufacturing private sector PMI fell to 49.5 in October from 50.6 in September. GDP in Q3 expanded by 4.9% from a year ago, above the 4.4% expected. In the first nine months of 2023, China’s economy has grown by 5.2%, which aligns with its 5% target. Much of the growth is from consumer spending, unleashed after the zero COVID policy changed in December of last year.

Keeping the 5% growth for next year could be a problem. With an aging population, the demographics are wrong. There continues to be an oversupply of housing and decreasing values. Foreign investors have sharply reduced their investments because of strict changing regulations. China is also experiencing deflation, a term we haven’t heard in ages, except for in Japan. Consumer prices fell 0.2% in October after staying flat in September. Exports have declined six months in a row, and housing is still deep in the doldrums. The Chinese government has no clear strategy or initiative to change and improve.

President Xi and President Biden meet this week. Maybe they can come to some resolutions on issues that could be productive for their countries.

Metals

Boring

The UAW (United Auto Workers) strike was finally settled, and average wages will increase 25% over the next three years. The Big 3 have been highly profitable over the last three years, and the unions were able to take a share of it. The other non-union auto makers, mainly in the south, will also raise their wages to keep the unions out.

China’s influence on the metals market remains minimal. While metals-related real estate demand is reeling, other sectors of China’s economy are picking up the slack to some extent. Specifically, there is decent metal uptake in EVs (Electric vehicles), electric cables, power grids, and solar and wind turbine production. With China still producing a surplus of most metals, prices remain flat.

November metals yawned. From July to November, prime and scrap prices have changed by only 3%. Steel prices rose 8% this month. The steel mills are running at an annual rate of 75%, down from last year’s 78%.

Thanks to Edward Meir of Marex for providing the latest 2024 Reuters forecasts for the cash price averages and inventory surpluses.

Cash Aluminum: $2,350, with a 250,000-ton surplus

Cash Copper: $8,625, with a 302,500-ton surplus

Cash Nickel: $19,270, with a 205,000-ton surplus

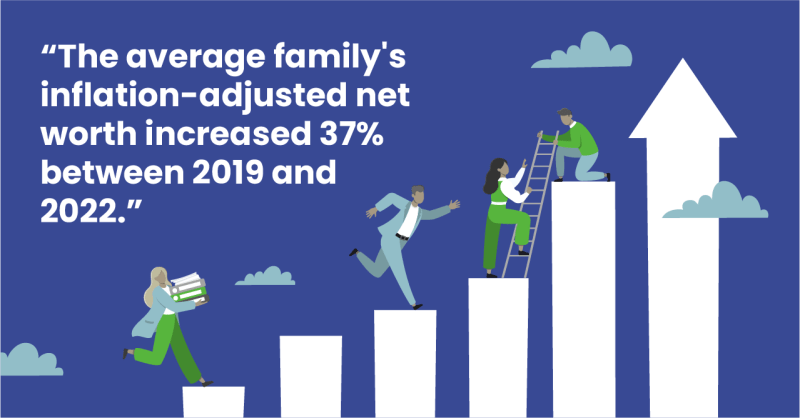

With all the chaos in the world and at home, the U.S. consumer keeps spending and driving the economy. We can all be thankful the U.S. economy is the strongest in the world and anyone who wants to work is working. The average family’s inflation-adjusted net worth increased 37% between 2019 and 2022. And these gains were felt across almost every sector of the population!

I wish you all a Happy Thanksgiving. Thank you for reading Market Insights and for your warm comments.

P.S. I have added a new segment at the end of each month’s Market Insights. It aligns with Shapiro’s purpose of Making the Planet Better Together. Shapiro has launched Circular by Shapiro (circularasaservice.com) to provide the environmental metrics and data needed to reach sustainability goals. Below, you will find Sustainability Insights.

Sustainability Insights by Maddie Carlson

29% of Emissions Come from Transportation

Required emission reporting is right around the corner.

There is still much confusion about what to report, let alone how to calculate emissions. To expand on last month’s Market Insights, using a mix of meaningful internal data and reputable external sources, these calculations are easier to manage.

The Environmental Protection Agency states that 29% of emissions come from transportation. Whether it is employee commuting or distribution, following the calculation below, manufacturers can quantify a substantial portion of their emissions.

Total Trip Miles ÷ Average Miles Per Gallon = Total Gallons

Total Gallons ÷ EIA’s* lbs. of CO2 Per Gallon of Diesel (22.45) or Gas (19.37) = Total lbs. of CO2

Total lbs. of CO2 ÷ lbs. Per Metric Ton (2,204.64) = Total Metric Tons of CO2 Per Trip

*US Energy Information Administration

Investigating these numbers will not only give reporting outputs but will highlight inefficiencies. Gathering a baseline and then working to cut idle time, maximize payloads, and eliminate redundant business travel would amount to an impactful sustainability report and strategy.

Call us, we are here to help. Info@shapirometals.com

“Thanksgiving Day is a good day to recommit our energies to giving thanks and just giving.“ —Amy Grant.

“Life is good. Family and health are precious.”

Bruce Shapiro

Comments are appreciated. If there are other people you know that would like to read this, please forward so they can subscribe below. This report was prepared by Bruce Shapiro and reflects my current opinion of the economy. It is based on sources and data I believe to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice.

Thanks for Reading.

Not a subscriber? Sign up below.