Market Insights

What Really Caused Inflation | June 2023

Market Insights

Market Insights

June 16, 2023

Shapiro - June 2023 Market Insights

Ben Bernanke, former chair of the Federal Reserve, and Olivier Blanchard, former chief economist of the International Monetary Fund announced their 2-year study on inflation. Bernanke is now at the Brookings Institution and Blanchard is at the Peterson Institute for International Economics. The two are among the world’s most cited academic economists. Blanchard was one of the few economists, along with Larry Summers who were the first to forecast inflation when the stimulus programs began.

Pandemic-related supply shocks explain why inflation shot up in 2021. An economy overheated by fiscal stimulus and low-interest rates explains why it has stayed high ever since. Their conclusion: For inflation to fade, the economy has to cool off, which means a weaker labor market.

“Monetary actions affect economic conditions only after a lag that is both long and variable,” said the great monetary theorist Milton Friedman. Fed Chairman Jerome Powell has quoted Friedman on this many times. The Fed has raised the interest rate to 5% in the last 15 months, and inflation has dropped to 4%, but not close enough to the 2% goal.

Higher interest rates have not substantially slowed labor demand. May’s job openings were up by more than 400,000 to over 10 million again, with only 5.7 million people available to work. The calculus to drop inflation to 2% by slowing the economy while raising the unemployment rate to close to 5% doesn’t add up to me. However, Bernanke and Blanchard believe that slowing the economy may be possible without raising unemployment so much. They use the ratio of vacancies to unemployed to measure labor market tightness. Amazingly, since late 2022, vacancies have dropped by about 20%, with only a slight rise in unemployment. The road to accomplishing this soft landing will happen with a considerable amount of my favorite acronym, VUCA.

Breaking news. At least to me.

New research from the Federal Reserve Bank of San Francisco reveals evidence that the labor market was never at the heart of the inflation problem anyway. Labor-cost growth has had a “small effect” on inflation, both overall and in the non-housing services category, where labor is a big proportion of company costs. The analysis found that recent increases in the employment cost index explained about 0.1-percentage point of the 3-percentage point increase in core personal consumption expenditures inflation. Who knew? I am still shaking my head as I try to digest this.

What else is causing inflation: rockets and feathers

When inflation started rocketing a few years ago, the reasons for raising prices were supply chain disruptions, logistics, the Putin war and higher gas and commodity prices. Large corporations, food chains, new and used cars, and durable goods manufacturers all raised their prices. We saw new and used cars prices and housing prices rise fast.

Now commodity prices and especially oil prices have fallen: gas prices were over $5 and are now down 40%. Logistics costs are back to pre-pandemic levels and there has been none of the dreaded wage price spirals. With all of that, prices have been falling like feathers at the grocery stores, restaurants, travel and on durable goods. Corporate profits are up and their stock prices are higher. Many companies have found that they can continue raising their prices without losing customers amid solid demand, at least for now. This could keep inflation too hot for some time and cause the Fed to tighten even more.

Inflation

Inflation measurements signal improvements.

- The Consumer Price Index (CPI) for May fell to 4.0% from a year earlier and down 0.9% from last month, which is the lowest in 2 years. The core CPI, excluding food and energy, eased to 0.4% in May, in line with expectations, and still higher than the 2.0% target.

- Super Core inflation, the Fed’s new preferred PCE sub-indicator, services only (no goods), excluding food, energy, and housing, increased 0.2% in May after rising only 0.1% in April. In the last twelve months, prices in the Super Core category are up 4.6%, versus 4.0% in the overall index, and 5.3% in the “core” index.

- Producer Price Index for May fell sharply. Annual price increases seen by producers measured 1.1% for the 12 months ended in May, falling from the 2.3% bump recorded in April. Driven by a decline in energy prices and food prices, this inflation measure has now decelerated for 11 consecutive months. It’s now at its lowest annual reading since December 2020, when post-pandemic demand was starting to return and producer prices were beginning their upward inflationary march.

- Personal Consumption Expenditures [PCE], the Feds preferred tool for measuring inflation, rose 0.4% in April, up from 0.1 in March, raising the twelve-month comparison up to 4.4% from 4.2% in March. Core prices, which exclude food and energy, pushed the twelve-month comparison up to 4.4% from 4.2% in March.

- Actual shelter/rent inflation remains very high. However, we know from the forecasts and the way inflation is calculated that it is dropping. We will soon start seeing shelter disinflation in the CPI and PCE in the months ahead.

Manufacturing

The ISM manufacturing index for May fell to 46.9 from 47.1 last month and is still in contraction. Fabricated metal products were one of 4 indices that reported growth in May, while 14 indices were down. The New Orders Index remained in contraction territory at 42.6 percent, 3.1 percentage points lower than April. The Production Index rose to 51.1. The Prices Index fell a whopping 9 points.

- Industrial production for April rose 0.5%. The biggest contributor to the gain in April was the manufacturing sector where activity rose 1.0%, with auto output soaring 9.3% and the rest of the manufacturing sector gaining 0.3%. Capacity utilization at factories increased to a 15-year high of 79.2%.

- ITR Economics US Total Industry Capacity Utilization Rate 1/12 was flat from March to April. The general decline in the rate signals that the US industrial sector will remain on the back side of the business cycle into at least the fourth quarter of this year. The decline will be mild due to stable consumer and business finances, backlogs, and onshoring trends. It then calls for the 12 month moving average (MMA )to rise in 2025.

- Shipments of “core” non-defense capital goods ex-aircraft (an essential input for business investment in calculating GDP and a leading manufacturer indicator) rose 0.5% in April after being down in March, and, if unchanged in May and June, would be up at a 1.2% annualized rate in the second quarter versus the Q1 average. We are still growing but at a smaller pace.

- Orders for core capital goods (excluding aircraft and transportation), which will lead to shipments in the future, were down 0.2% after being up slightly in March. In the past year, orders for durable goods are up 4.2%, while orders excluding transportation are down 0.2%. After factoring in the inflationary rise in producer prices for capital goods, orders declined when adjusted for inflation.

- Automakers sold cars and light trucks at a 15.0 million annual rate in May, down 6.5% from April but still up 19.6% from a year ago. In addition, sales of medium and heavy trucks hit a 558,000 annual rate in May, the fastest pace since 2019.

- New home sales were up 4.3% despite 7% 30-year mortgage rates. Home prices have moderated and inventories, while still low, have grown. This is partly due to the low inventory of existing home sales because owners don’t want to give up low-interest rates.

- US Nonresidential Construction Contracts Index fell 28.74% from a record last month but is still up 10.72% from one year ago. This includes commercial projects, including highways, hotels, and hospitals.

- The Shapiro Nonferrous Scrap Activity Index for May, which tracks our daily purchases from the same accounts across our 10 locations and a diverse industrial base, rose from April and is 6% over our 12-month trailing average.

China and the world

China’s official PMI fell in May to 48.8 from 49.2. The private Caixin rose to expansion for the first time in 5 months. Services also fell but are in expansion. Housing continues to be a big problem and it will be for some time. Youth unemployment for those under 25 is 20%. Car manufacturers produced 2.13 million units in April 2023, down a sizable 17.5% month over month while car sales were down 12% year over year.

Publicly, the Chinese people follow what the government says they should do. Privately it is another story. The zero Covid policy has changed consumer confidence. Its impact will be felt for many years. Even when the government comes out with a new stimulus package, the Chinese economy will be slow for some time.

Europe saw 2 quarters of negative grow and is officially in a recession. Inflation is falling along with energy prices. The German economy, which is the manufacturing powerhouse of Europe had negative growth and is also in a recession.

The US is fortunate to have such a strong economy.

Metals

With the slowdown in China and Europe, metal prices remain soft. The Aluminum Association reported Q1 demand for aluminum in North America fell 3.5%, while the semi-fabricated – or “mill” – product demand was off 7.3% year-over-year through the first quarter. Extruded products have been down over double digits in Q1. Index of Net New Orders of Aluminum Mill Products shows a decline of 8.2% year-to-date. It is no surprise that prime aluminum prices and scrap fell again this month. Secondary prices were steady. Stainless steel, copper and steel prices were also weak and down close to 10% from May.

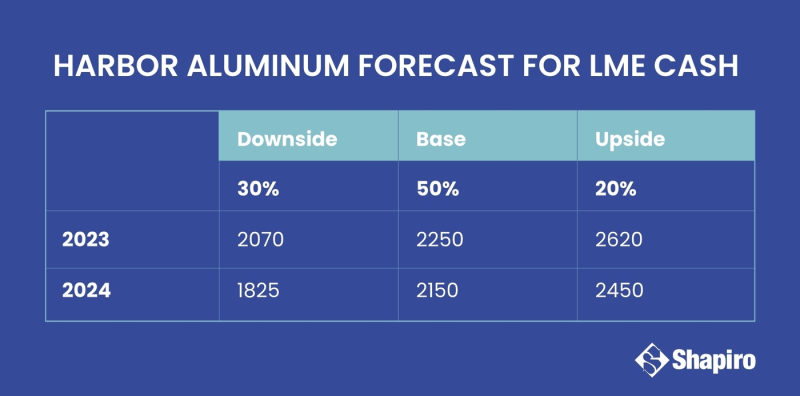

Harbor’s 15th Annual Aluminum Summit was held last week. The content and the people make it the premier event to attend. Their forecast from last year was spot on. Their aluminum forecast for LME cash for 2023 and 2024 is:

Great manufacturing news

Construction spending as a % of GDP has more than doubled since the Inflation Reduction Act (basically an infrastructure act) and the CHIPS Act were passed a little over a year ago. The total dollars spent rose from $800 billion annually 10 years ago to over $1.8 trillion currently. Annual spending should be close to $1.7 trillion over the next 5 years. This does not include the equipment that will be needed in these factories. These projects will also include many new jobs. The US will not get back to the 25% manufacturing portion of the 1970’s but this is still excellent news for us.

Circular futures for leaders in US manufacturing

As we chart the future of manufacturing, Shapiro is in a unique position to lead the sector towards processes where environmental stewardship and economic value work together. Shapiro’s services for OEMs offer clear ESG reporting, circular supply chain management, and tailored master alloy programs. Circular services and solutions allow manufacturers to weather and thrive in the complexities of today’s market. Growth trends in manufacturing suggest this is the time to integrate future-forward strategies. Reach out to Shapiro’s sustainability experts’ to accelerate a sustainable future for your corner of the manufacturing industry.

"Nothing will ever be attempted if all possible objections must be first overcome."

Thanks for Reading.

Not a subscriber? Sign up below.

Comments are appreciated. If there are other people you know that would like to read this, please forward so they can subscribe below. This report was prepared by Bruce Shapiro and reflects my current opinion of the economy. It is based on sources and data I believe to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice.