Market Insights

The Conundrum & Changing the Calculus | February 2023

Market Insights

Market Insights

February 15, 2023

February 2023 Market Insights

The Fed's conundrum

How high do interest rates need to go, and how long to cool the economy and inflation while not causing a hard landing? The Fed is trying to navigate these very tricky waters.

Paul Krugman writes, “I sometimes think of the Fed as trying to operate heavy machinery in a dark room — while wearing heavy mittens.”

On February 1, as expected, the Fed raised interest rates by 0.25%, slower than the December 0.5%. “We’re talking about a couple of more rate hikes to get to that level we think is appropriately restrictive,” Fed Chair Powell said after the central bank’s policy meeting.

Wages, price growth, and inflation have been moderating over the last few months. “We’re going to be cautious about declaring victory and sending signals that the game is won,” Powell said. He continued, “but our forecast is that it will take some time and some patience and that we’ll need to keep rates higher for longer.”

PCE, personal consumption expenditures, is the Fed’s preferred measure of inflation. This gets kind of wonky, but there is a subset of this narrower measure called the supercore.

The supercore is services, excluding food, energy, and shelter. In December, annual supercore inflation was running at about 4%, below inflation of 5% but still double the Fed’s 2% target.

About 60% of that is related to the labor market. With the tight labor market, Mr. Powell said inflation won’t return to 2% “without a better balance.”

And then, two days later, the January jobs report came out with a whopping increase of 517,000. Is this the start of a new growth trend or an anomaly? I lean towards anomaly but with a stable economy. More on that below.

The economy and the recession

GDP grew at 2.9% in Q4. Half of this growth was due to inventory restocking as companies transitioned their strategy from just-in-time to just-in-case. Consumer spending was also strong, as was government spending. However, most forecasts for 2023 put GDP around 1%, with inventories and spending retreating.

Despite the tech companies and other large companies announcing layoffs, small companies, who employ less than 250 people, have been responsible for all of the net job growth in the United States. This is the case since the onset of the Covid-19 pandemic can account for almost 80% of the available job openings.

Jobs. Jobs. Jobs.

January employment grew by 517,00 with solid growth in services and health care. This number far exceeded any forecasts. The unemployment rate dropped to 3.4%, last seen in 1969. Meanwhile, the latest number for job openings increased by an amazing 572,000 to over 11 million, the tenth month out of the last 15 openings has been north of 11 million. This has happened with the wage increase going lower.

There are now 2.8 million more people working than in pre-pandemic estimates. Most of these new jobs are in professional and business service, education, transportation, warehousing, education, and health. Yet, there are still over 1 million fewer people working in leisure, hospitality, and government than pre-pandemic estimates.

The economy will slow with the higher interest rates, but this job situation is a significant conundrum. If this employment imbalance continues for a long time, so will inflation.

"...it's an election year so don't believe everything, or most likely anything, you hear."

Bruce Shapiro

Inflation and the recession

The CPI rate of inflation continues to moderate. Shelter, which is a third of CPI, was higher, partly due to the way it is measured. It eventually will start falling. Services continue to rise with the cost of medical care, dining out, hotels and transportation. The higher wages needed to support these industries are not going away.

Inflation is high but I have seen a lot worse. In June 1980, inflation was 14% and unemployment was 7.6%. Paul Volcker raised interest to 20% and it took a few painful years for him to break the wage price spiral. He finally did and declared that inflation was cured when it got down to 4%.

Keeping interest at 5% sounds high to many people. They complain that it is killing the economy and will cause a hard landing.

We can avoid a wage-price spiral and find a soft landing.

Larry Summers, Secretary of the Treasury from 1999 to 2001 and Director of the National Economic Council from 2009 to 2010, forecasted inflation long before most did. He believes it will take much higher interest rates and years to bring inflation back to 2%.

“If we fail to deal with inflation, we are likely to have a more severe recession at some point.” -Larry Summers

- Consumer Price Index (CPI) fell for January to 6.4% from December’s 6.5% year-over-year rate. The core CPI, excluding food and energy, eased to 5.6% on an annual basis from 5.7%. On a monthly basis the base CPI was up 0.5% and core prices were up 0.4%. These were in line with estimates.

- Personal Consumption Expenditures (the Feds preferred tool for measuring inflation) rose 0.1% in December and are up 5.0% from a year ago. This is down 0.5% from last month. Core prices, which exclude food and energy, rose 0.3% for the month and are up 4.4% from a year ago but still down from November’s 4.7%. The supercore subset is moving in the right direction. January PCE report comes out at the end of the month.

- The Producer Price Index for December (January is out on Thursday) fell the most for any single month since April 2020. Falling costs for food and energy more than offset rising prices across most other categories. This is no surprise as the economy shifts from buying goods to buying services. Energy fell sharply by 7.9%, and food prices fell by 1.2%. Core prices for goods and services were up slightly and have been trending down. I expect January to be up.

Manufacturing

The ISM manufacturing index for January fell further into contraction to 47.4. Of the 18 measurements used to determine ISM, 16 were down again, the same as last month. The prices paid index rose from 39.4 to 44.5. Supply chain issues are improving even though new orders are dropping. Also, employment is increasing.

There are other slow-down signs in manufacturing.

Industrial production fell 0.7% in December and is now down 5.2% at an annualized rate in the past three months. This is the worst three-month reading since the early days of the COVID pandemic. The manufacturing sector was the biggest contributor to today’s negative headline number, with production falling by 1.3%.

- Shipments of “core” non-defense capital goods ex-aircraft (an essential input for business investment in calculating GDP and a leading indicator for manufacturers) declined by 0.4% in December but are up 5.1% annually in Q4. This helped the GDP attain 2.9% in Q4.

- Orders for core capital goods (excluding aircraft and transportation), which will lead to shipments in the future, fell 0.2% after being up the previous two months.

- Light vehicle sales for the year dropped to 13.7 million units. The chip problem is still to blame. January sales were up almost 18% from December and are at 15.7 million units annualized rate.

- Aircraft production was 7.9% higher in 22 than in 23 and is forecast to be up again this year. Farewell to my favorite plane, the 747, after over 50 years of production.

- The Shapiro Nonferrous Scrap Activity Index for January, which tracks our daily purchases for the duplicate accounts across our 10 locations and a diverse industrial base, fell 2% from December and down 5% from our 12-month trailing average.

China

China is reopening.

The official PMI manufacturing index for December rose from 47.0 in December to an expansion territory of 50.1 in January. China accounts for about half of the global gross domestic product growth this year. Economists predict that China’s economy will expand by nearly 5% in 2023, ahead of the 3% growth registered last year. For the Lunar New Year, billions of people traveled after two years of lockdowns and severe restrictions.

Just as in the US in 2021, after the vaccinations and the stimulus money was available, spending on goods took off. With it came the bottlenecks and supply chain issues. The Chinese vaccine is not as good, and millions could die. Even though the real numbers will not be reported, China will recover this year. The growth will be gradual because the Chinese have just lived through a few years of lockdowns and unemployment.

Many will fear the future and tend to hold back their spending.

The government will be doing more to increase employment, especially with the much higher youth unemployment at 18%. Housing is 30% of the GDP, and there is still an issue with oversupply. Gregory Wittbecker, at the recent Platts Aluminum meeting, pointed out the Chinese Hokou housing policy, which limits individuals to purchasing property only in the city where they were born. This policy restricts 400 million Chinese, and it severely reduces the demand in many of the upper-tier cities. If this policy is changed, the sale of properties will increase. This will help reduce the surplus of unsold homes and cause a surplus of rentals. The government has yet to announce its policy.

Chinese construction is a powerful worldwide driver of metals.

The downside of China’s reopening will be the increase in worldwide inflation as consumption increases. Such is life.

Things are also picking up in Europe. The IMF is now calling for growth there of 0.7%, which is much better than last year’s forecast.

There has been great news with the mild winter there and the decreased need for energy. Natural gas inventories have gone up from worldwide shipments, and the price has dropped to pre-pandemic prices. Europeans are used to high energy prices and conservation. The Putin war has taught them an important lesson about who they depend on for energy.

Green technology will continue to grow rapidly in Europe.

Metals

January’s primary aluminum metal prices continued to rally despite the current slowdown in consumer buying.

A good part of the increases was due to the anticipated demands with the reopening of China. The dollar is weaker. The winter in Europe was milder, and the energy supplies there are abundant enough to offset the diminished supplies from Russia. Inflation is slowing down, and the forecast for the rest of the world is looking better. The International Monetary Fund (IMF) has raised its worldwide growth for GDP to 2.9%.

Metal inventories have also fallen. Aluminum stocks at the end of December on the London Metal Exchange were over 50% lower than at the beginning of 2022. They crashed from more than 900,000 tons to 447,250. Aluminum stocks at the Shanghai Futures Exchange also finished the year sharply lower. Copper stocks are also very low. While all that was true for January, prices for aluminum, copper and nickel are off so far in February.

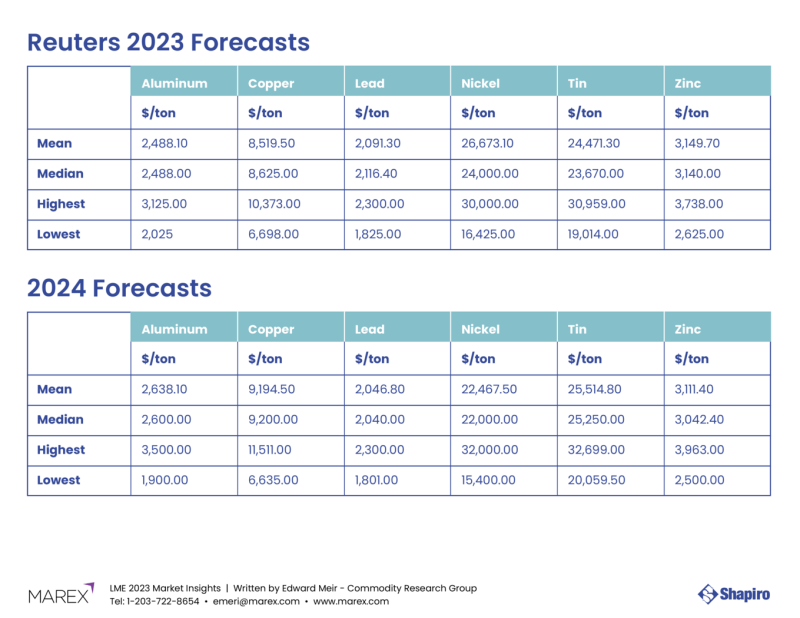

One of the best metals forecasters I know is Edward Meir. At the beginning of every year, he puts together his annual forecasts. “This past year was among the most volatile and unpredictable of the many we have reviewed in our time covering commodities. Pretty much everything that could have come our way (short of the “Ten Plagues”) was thrown at us. This includes an unexpected war in Ukraine, soaring inflation, a spike in global interest rates, lingering supply-side issues, slowing growth, and an increasingly fraught geopolitical world order. Even COVID reared its head late in the year after China threw in the towel on its lockdowns and decided to “uncork” the virus instead.” Ed pretty much nailed the 2022 forecast. I believe he reads tea leaves as a hobby.

Here is his 2023 forecast and his scorecard from 2022. Amazing.

Also, courtesy of Ed, is the Reuters poll on metals for this year and next came out at the end of January. You can see what the other forecasts are.

Harbor Aluminum, another well-respected firm that I have followed from its very start, has a base LME Cash price forecast for 2023 of $2,100 per metric ton. Their aluminum 2022 forecast was also very close.

Following forecasts is one of my favorite hobbies.

For those of you who haven’t read Market Insights before, VUCA is the rule– Volatility. Uncertainty. Complexity. Ambiguity.

It will continue to keep changing the calculus. I hope this helps you make your buying and selling decisions. At Shapiro our strategy continues to be to minimize our risk by matching our purchases with our sales and hedging any open positions.

“You either win or you learn.”

Jalen Hurts

Life is good. Family and health are precious.

Bruce Shapiro

Comments are appreciated. If there are other people you know that would like to read this, let me know and I will add them to our distribution list. This report was prepared by Bruce Shapiro and reflects my current opinion of the economy. It is based on sources and data I believe to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice.

Thanks for Reading.

Not a subscriber? Sign up below.