Market Insights

Tariffs: Yes, The Price Was Too High | May 2025

Market Insights

Market Insights

May 16, 2025

May 2025 Market Insights

My April headline was Tariffs: A Price Too High? Surprise! The answer was YES.

Monday’s early morning flip flop, roll back, announcement was a big surprise. Trump rescinded the 145% tariffs to 30% and paused implementation for 90 days. The 30% rate is still much higher than the 10% tariffs on the rest of the world. China matched the roll back in tariffs on the U.S. which basically stopped exports from China. They will now start up again, however, there will be delays in shipments and restarting production before things return to normal.

The 30% tariff is still high. Estimates are that this rate will reduce exports from China by a minimum of 33%. Those tariffs will still be inflationary.

China did agree to the removal of seven rare earth minerals from its export control list. Securing the elimination of those restrictions was a priority and a win for Washington defense industries and a part of U.S. security.

This is still just a pause in uncertainty. Negotiations will take months to finalize. As we have been witnessing, unpredictability and chaos will continue for months, maybe years.

Saturday, which seems like ages ago, I wrote the following:

Trump believes that tariffs will reduce our trade deficits, protect American jobs, encourage domestic manufacturing, and increase our national security. We will see. Here is a brief timeline of what has happened since Liberation Day.

- April 2 - Liberation Day. Trump announces tariffs on every country in the world with “no exceptions” starting April 9.

- April 9 - As the stock markets react to Liberation Day and continue crashing, Trump declares a 90 day pause on implementing the tariffs on all countries except China, which has a 145% tariff on all goods.

- April 13 - Trump exempted Chinese tariffs on smartphones, computers, laptops, memory cards, semiconductor devices, and flat panel displays. Those tariffs would have more than doubled the price of those items.

- April 21 - Trump met with the executives from Home Depot, Target, Walmart and other big box stores. They told him that if the Chinese tariffs continue, store shelves will be empty of most Chinese imported products in 2 months.

- April 29 - Amazon announced it planned to show shoppers how much of their bill is owed due to the tariffs. The White House press secretary responded to this and said the company was parroting Chinese propaganda.

- April 29 - Later in the day Mr. Trump said he had spoken with Amazon founder Jeff Bezos, who he said, “solved the problem very quickly.” Looks like we won’t know the true costs of tariffs.

- April 30 - This was Trump’s 100th day in office. Stocks logged their worst 100 days of any President since Nixon dropping 7.1%. Since that low point in early April, and the China tariff pause, stocks have recovered.

- April 30 - WSJ Editorial Board wrote “The best response to the warning from the first-quarter GDP decline would be for Mr. Trump to call the whole tariff thing off. Short of that, settle for 10% across the board and call it a day.”

- May 8 - WSJ Editorial Board “Trump Stages a Trade War Retreat.” The first trade deal was signed with Great Britain. The details needed to be worked out, but the deal marks another step back from tariff uncertainty.

- May 9 - The U.S. and China began tariff negotiations in Switzerland.

- May 12 - Breaking News! Trump rolls back 145% China tariffs to 30%.

Tariff Uncertainty

The Economic Policy Uncertainty Index has climbed to its highest point ever as of May 8. It is 33% higher than its previous Covid 2020 high. It reached 4900 on April 11th and fell to 2900 as of May 8th, still a record high, not including this year.

As Fed Chair Jerome Powell said on May 7th at a news conference “If the large increases in tariffs that have been announced are sustained, they’re likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment.”

China uncertainty - Still lots of questions

China and the U.S. economies are crucial to one another. Negotiations started with China on May 9th. China has had a long-term strategy of making itself less reliant on the U.S. since Trump was first elected in 2016.

In 2020 China President Xi Jinping said Chinese leaders must “tighten international production chain’s dependence on our country, forming a powerful capacity to counter and deter foreign parties from artificially disrupting supplies.” This strategy is the key issue for the U.S. and the rest of the world. China’s objective is economic domination of the world.

"China’s strategy is to dominate the supply chains of products the world needs. That power reduces the effects of tariffs and dependence on the U.S. and other countries"

Bruce Shapiro

China is producing 30% of what the world needs while only consuming 15%. Selling those products at discounted prices causes many countries to put tariffs on Chinese goods so that it doesn’t destroy their economies.

Last year, the U.S. imported about $450 billion in products. 85% of this is used in manufacturing and 15% are consumer goods. Without these products manufacturing will be reduced. For example, the electric motors in all appliances and many are from China.

China has also imposed export restrictions on a wide range of critical minerals and metals. They supply 72% of rare earth minerals to the U.S. and large percentages of metals for assembling everything from cars and drones to robots and missiles. They supply 90% of rare earth magnets used in electric vehicles.

China relies on the U.S. exports for electronics (including semiconductors), aircraft, and pharmaceutical products. They import agricultural goods including oilseeds, grains, and soybeans and over the last 5 years have lowered their dependency on these goods.

Our economies are still codependent. President Xi Jinping rules China and controls everything. There are no elections in China. He can play a long-term strategy and will. China can suffer through the trade wars. If it gets too bad, there are numerous ways to stimulate his economy when and if he chooses.

Trump likes to make deals and is used to quick negotiations. The Chinese are patient and have always devised long term strategies. In 1898 China leased Hong Kong and the New Territories to the United Kingdom for 99 years. In 1997, they were returned to China. I expect tariff negotiations to continue for quite some time.

Tariff uncertainty has created chaos in a myriad of industries. Prices on commodities and retail items have been rising but have yet to show up in the inflation and manufacturing data.

The Volatility of policy change is constant. The Uncertainty and higher tariff prices are slowing our economy as businesses and consumers wait to see what the impacts are. The Complexity in decision making seems overwhelming. The Ambiguity adds to the chaos. And there you have it, VUCA, once again.

INFLATION

Tariff impact not in current data

- The Consumer Price Index (CPI) for April rose 0.2%. Year over year it up a modest 2.3%.

- Core inflation for April rose 0.2%. The annual rate year was 2.8%.

- Personal Consumption Expenditures, PCE, the Fed’s preferred inflation measure for March was unchanged from February and is plus 2.3% from a year ago. Core prices, which exclude the ever-volatile food and energy categories, were also unchanged from last month and plus 2.6% from a year ago. March is the latest data out and does not reflect the tariffs.

- The Producer Price Index for March decreased to 2.7% from 3.2% in February. April PPI will be out May 15.

Manufacturing

Tariff uncertainty is not showing up yet

China

Steady as she goes

China’s economy is starting to suffer because of the tariff trade wars. The April official PMI dropped into contraction to 49.0 from 50.5 last month. The private Caixin also dropped to 50.4 from 51.2, which is slightly above expansion. Most of the drop was again attributed to the tariffs.

While China’s economy will also be hurt by the trade wars, as mentioned before, President Xi has a long-term strategy. The Covid lockdowns occurred from January 2020 until December 2022. The housing crisis started in 2021 and still hurts. The population is falling, and unemployment is up. All of this hurts their economy.

As of the latest available data, China's exports are broadly categorized into manufacturing-related and consumer goods. Here's a general overview:

Manufacturing-Related Exports

Approximately 80-85% of China's total exports are related to manufacturing products. This includes machinery, electronics, industrial equipment, and intermediate goods used in global manufacturing processes.

Consumer Goods

Approximately 15-20% of China's exports are consumer goods, such as apparel, footwear, personal electronics, household items, and other finished consumer products.

Key Points

Electrical machinery and equipment remain the largest import category, often accounting for roughly 40-45% of total imports from China.

Furniture, toys, apparel, and automotive parts also represent significant portions.

U.S. goods imports from China in 2024 totaled $438.9 billion, up 2.8% ($12.1 billion) from 2023. The U.S. goods trade deficit with China was $295.4 billion in 2024, a 5.8% increase ($16.3 billion) over 2023.

I found this information to be interesting and surprising as well.

Metals

Tariffs uncertainty softens the market

Metal prices have been strong all year. The old expression “sell in May and go away” was a little early this year. After prices on all metals were on the upswing for four months, they fell in April after the Liberation Day announcement. They really crashed for the first week and then somewhat came back after the 90-day pause was announced. Prime aluminum was the big loser. From the beginning to end of April, the LME fell 5 cents, and the Midwest premium fell 3.5 cents. The PMTA fell 13 cents.

Prime aluminum scrap prices were down 10 cents. Secondary aluminum scrap fell from 2 to 4 cents. This was also impacted by the tariffs as virtually no scrap was going to China, and other Asian countries also cut back on buying. Copper fell close to $1.00 per pound to nearly $4.00 before it recovered and finished the month at $4.65. Stainless steel prices fell slightly, and steel scrap also dropped.

Nucor Steel had mixed reactions to the steel tariffs. They welcomed reduced imports but also complained about the tariff impact of raw materials they imported that increased their production prices.

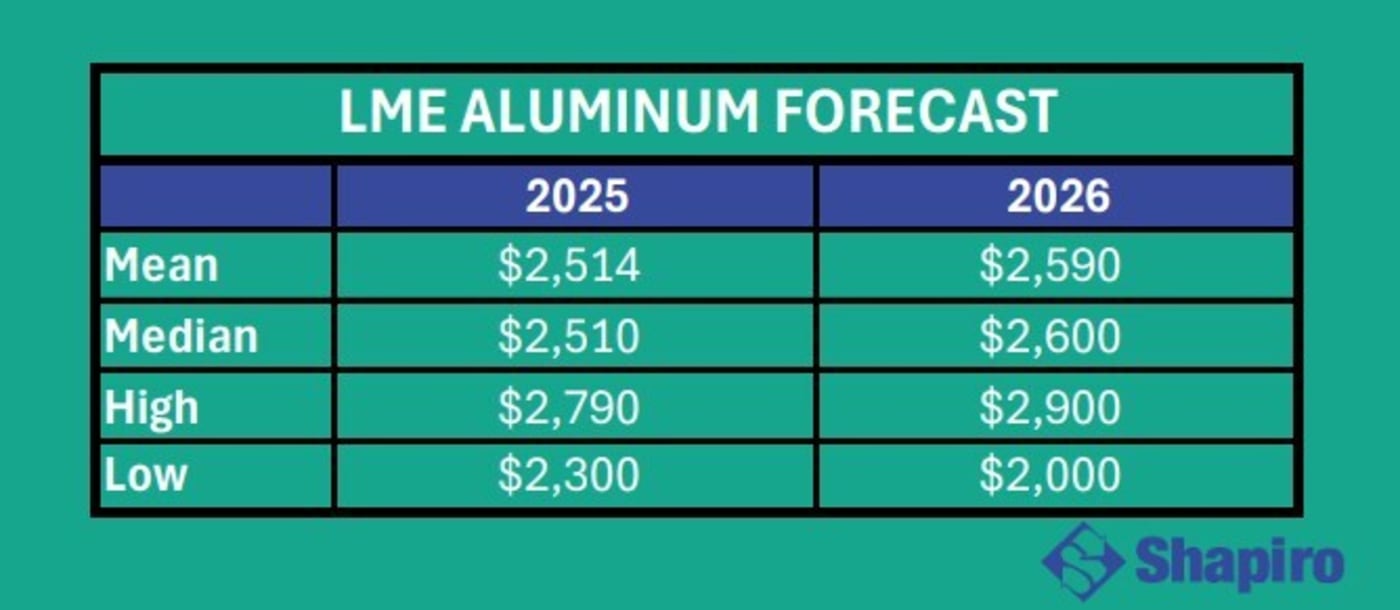

With all the uncertainty, Reuters aluminum poll for 2025 LME dropped by $60 per ton.

Conclusion

All month long, I consistently research and read a variety of economic periodicals including the Wall Street Journal, Bloomberg, the New York Times and Axios. I don’t watch or follow heavily slanted news media. I want to learn about both sides of the topics and issues I present. This gives the readers an opportunity to decide for themselves. Factuality is important to me.

In the future, much will be written about the facts surrounding the Liberation Day tariff trade wars and their political impact on trade relationships, global agreements and what happens next.

I also discuss the economy with both Republicans and Democrats. The Republicans either back what Trump is doing, have questions about his policies or say “we will see.” Most agree they would prefer less verbosity. I believe Teddy Roosevelt was right when he said “Speak softly and carry a big stick; you will go far.”

What do you think?

“One thing we have lost, that we had in the past, is a sense of pogress, that things are getting better. There is a sense of volatility but not progress."

Daniel Kahneman

Thanks for Reading.

Not a subscriber? Sign up below.